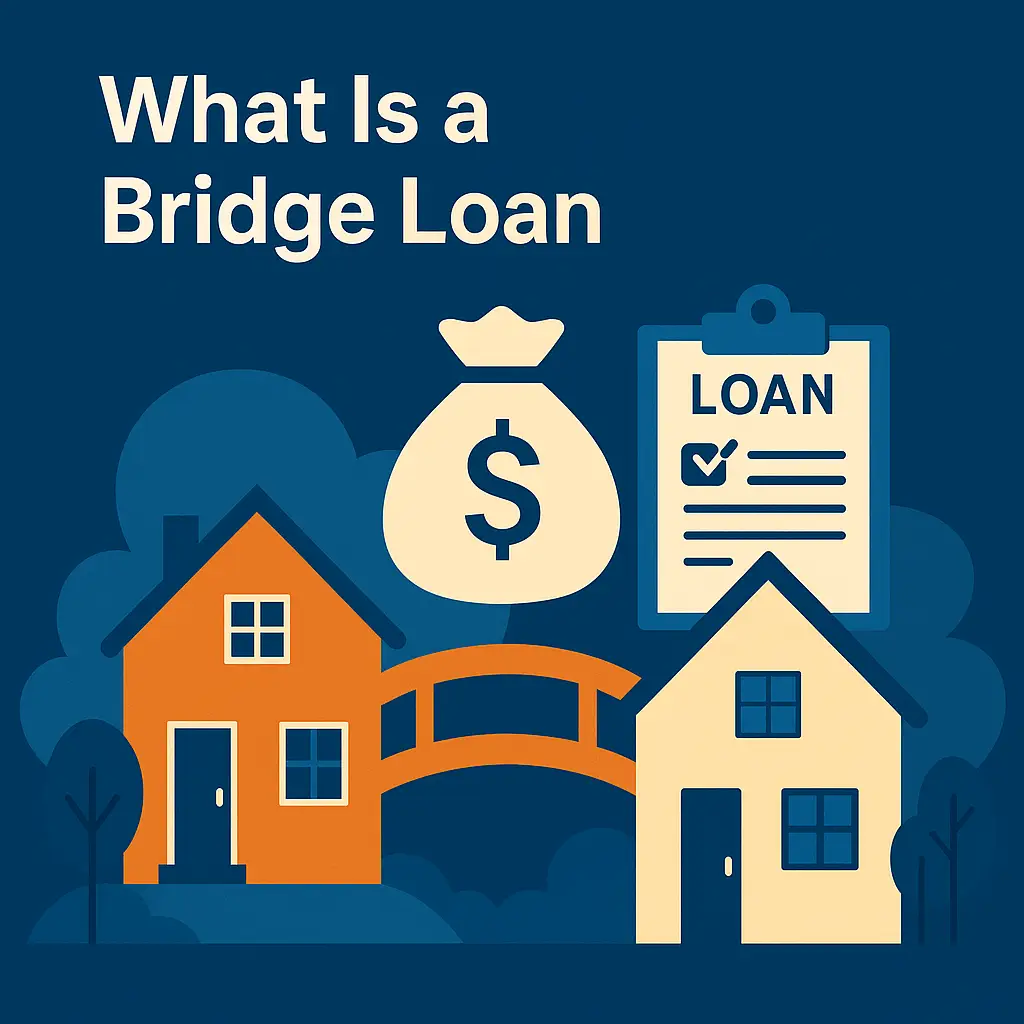

Moving between homes can be stressful, especially when you haven’t sold your current one yet. That’s where a bridge loan can make all the difference. But like any tool, it comes with its risks and limitations. Let’s break down what a bridge loan is, how it works, and whether it could be a smart move for your next mortgage venture.

Bridge Loans in a Nutshell

A bridge loan lets you finance a new home before your existing home sells. In a competitive market, this gives you the edge of making an offer without needing your old home’s sale first. But it’s designed as a short-term fix, not a long-term solution.

Quick facts:

- You can often borrow up to 80% of the combined value of your current and new homes

- Terms usually last between 3 to 12 months

- Interest rates and fees tend to be higher than conventional mortgages

- Works best in markets where houses sell quickly

How a Bridge Loan Works

Bridge loans differ from standard mortgages because they’re temporary. You use them to buy your next home using equity from your current one, without waiting for the sale. You’ll pay more in interest, but you gain flexibility.

There are two common ways people use a bridge loan:

- Pay off your current mortgage and use the rest as a down payment on the new home.

- Keep your existing mortgage and let the bridge loan cover the down payment on the new property.

Either way, the assumption is you’ll sell your current home soon. If it doesn’t sell before the loan term ends, you could be stuck juggling two mortgages plus the bridge loan. That’s a risky situation.

Typical bridge loans must be paid off within three months to a year. Lenders usually want a credit score above 700 and a debt-to-income (DTI) ratio below 50%. Some lender allow for no DTI ratios if the strategy makes sense. The combined borrowing limit often maxes out at 80% of the value of both homes.

Pros and Cons of Bridge Loans

Pros:

- You avoid placing a contingency on your offer

- With a down payment above 20%, you may bypass private mortgage insurance (PMI)

- Gives you breathing room to line up your next move without rushing the sale

Cons:

- Higher rates and closing costs than standard mortgages

- You may end up owning two homes temporarily

- Some lenders limit bridge loans to primary residences only

When a Bridge Loan Makes Sense

You might consider a bridge loan if you:

- Can’t make a compelling offer because sellers reject contingencies

- Don’t have a down payment without equity from your current home

- Find a house you love but haven’t listed your current one

- Face mismatched closing dates—your current home sale closes after your new home

How to Secure a Bridge Loan

Getting a bridge loan follows many of the same steps as a mortgage—but speed, equity, and credit matter more. Shop lenders who specialize in bridge financing, compare terms, and ask about fees and interest. Some lenders may require collateral or equity thresholds.

Bridge Loan Alternatives

If the risks feel too steep, other methods may offer more security:

- HELOC (Home Equity Line of Credit): Access your equity as a revolving line, often with lower rates

- Home Equity Loan: One-time lump sum with fixed payments

- 80-10-10 strategy: Combine first and second mortgages to avoid PMI and spread out costs

- Personal Loan: Though rates may be higher, this is unsecured and not tied to your property

How to Secure a Bridge Loan

Getting a bridge loan follows many of the same steps as a mortgage—but speed, equity, and credit matter more. Shop lenders who specialize in bridge financing, compare terms, and ask about fees and interest. Some lenders may require collateral or equity thresholds.

How to Secure a Bridge Loan

Getting a bridge loan follows many of the same steps as a mortgage—but speed, equity, and credit matter more. Shop lenders who specialize in bridge financing, compare terms, and ask about fees and interest. Some lenders may require collateral or equity thresholds.

Getting a bridge loan follows many of the same steps as a mortgage—but speed, equity, and credit matter more. Shop lenders who specialize in bridge financing, compare terms, and ask about fees and interest. Some lenders may require collateral or equity thresholds.