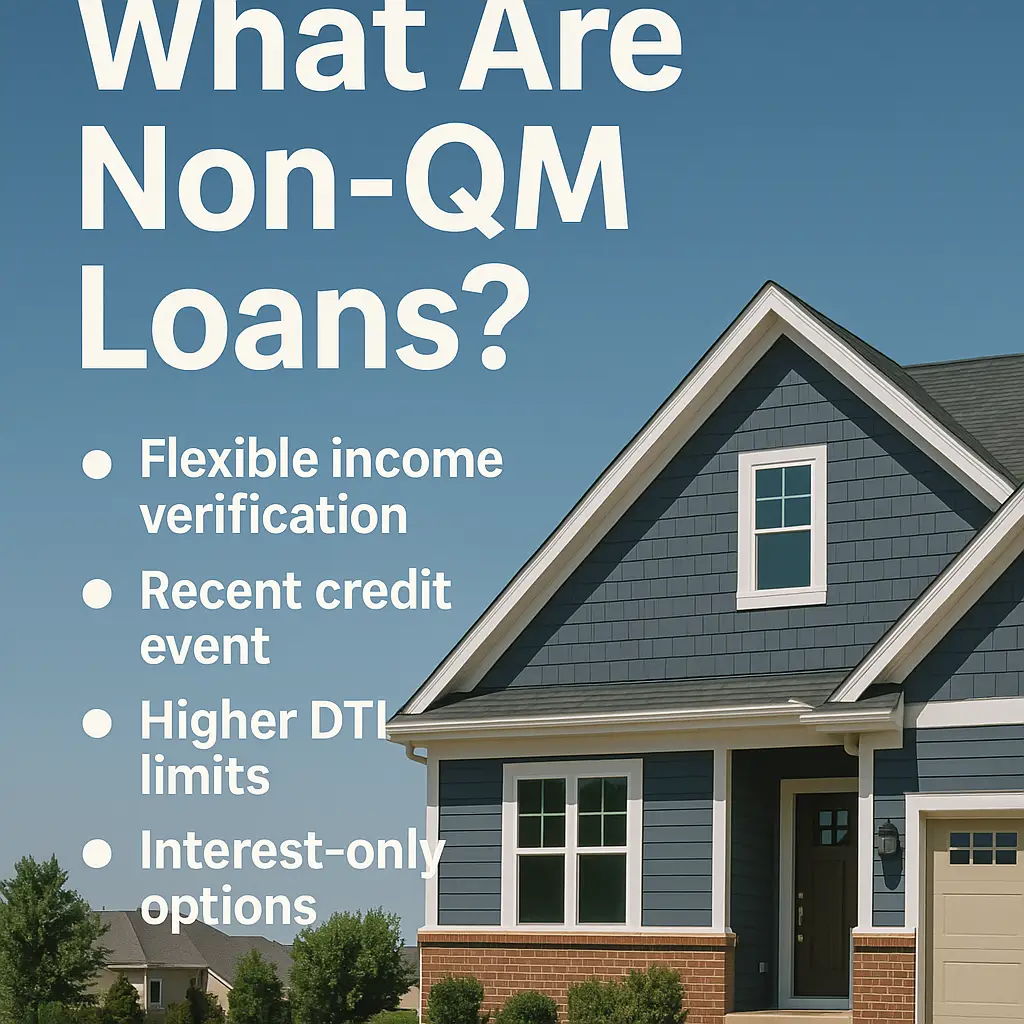

What Are Non QM Loans?

When you are creditworthy yet do not check all the boxes for a traditional mortgage, a non QM (non-qualified mortgage) offers a path forward, though it often comes with trade-offs. Unlike standard qualified mortgages, non QM programs allow lenders to approve borrowers who cannot use conventional income proof methods. Because they carry higher risk, these loans tend to demand higher rates and stricter terms.

Many borrowers end up in this space simply because they lack W-2s or regular pay stubs. Whether you’re self-employed, a retiree, or an investor relying on rental income, non QM loans open doors that conventional mortgages often keep closed.

What Makes Non QM Loans Different?

Non QM loans are built for borrowers whose financial profiles do not align neatly with traditional lending. Common features include:

- Alternative income documentation such as bank statements, 1099s, or profit and loss statements

- No waiting period after bankruptcy or foreclosure in some cases

- Higher debt-to-income (DTI) ratios allowed, often going above 50%

- Larger down payment requirements (15% to 20% or more)

- Higher interest rates to compensate lenders for added risk

- No government backing. These loans can’t be guaranteed by Fannie Mae, Freddie Mac, FHA, VA, or USDA

Also, non QM loans may include interest-only repayment options. That can lower monthly payments early on, but you must understand that your principal does not decrease until you begin amortizing.

Who Should Consider a Non QM Mortgage?

If any of the following describe your situation, non QM may be a good fit:

- You’re a contractor, self-employed, or working gig jobs and cannot provide traditional income documents

- You’ve had a recent credit event like bankruptcy or foreclosure

- You’re a real estate investor or landlord and want to use cash flow from rentals to qualify

- More than 43% of your income goes toward debt

- You need flexible mortgage solutions that traditional loans will not allow

Popular Non QM Program Types

Many non QM lenders offer a variety of program types. Here are a few you may see:

- Bank Statement Loans — Use 12 to 24 months of personal or business bank statements to prove income rather than relying only on tax returns

- DSCR Loans (Debt Service Coverage Ratio) — Let your investment property’s cash flow qualify you; this is popular for fix-and-flip or rental investors

- 1099 / P&L Programs — Ideal for contractors or freelancers who receive 1099 income or have strong profit and loss statements

If you want to explore whether a flip property will be profitable, try our Fix and Flip Calculator

To estimate eligibility via cash flow for DSCR deals, check our DSCR Calculator.

Some of these loan programs can also link directly to your business or purchase. Check out our Product Page

Weighing the Trade-Offs

While non QM loans provide valuable flexibility, they also demand extra diligence:

- Higher interest and fees increase your long-term payments

- Larger equity requirements to safeguard lenders

- Lenders may demand stronger credit or collateral

- Repayment risks, especially under interest-only terms

That said, for many nontraditional borrowers entrepreneurs, real estate investors, or those recovering from credit events non QM can be a powerful option when traditional paths close off.

Non QM loans are a lifeline for borrowers who do not fit the mold of traditional mortgage underwriting. While they come with steeper costs, they also provide remarkable flexibility. Whether you need a bank statement loan, a DSCR solution, or a 1099 / P&L program, options exist when conventional paths are closed.